The data presented in this example vignette is inspired by a study from Anandarajan et al. (2002), who looked at the impact of communication means through different disclosure format on the perceived risk of organization on the brink of bankruptcy in accountancy. There is a single between-subject factor for the disclore format, and three measures of the performance, ratings for the interest rate premium assessed, for the ability to service debt and that to improve profitability.

Data

We first load the data from the package and inspect the content.

The data are unbalanced by condition. In general, we need them to be roughly balanced to maximize power. The manova function will not be usable unless data are balanced, and we need to enforce sum-to-zero constraints to get sensible outputs. After this is done, we can fit the multivariate linear model with lm by binding columns on the left of the ~ sign to gather the response vectors.

Code

options(contrasts =c("contr.sum", "contr.poly"))model <-lm(cbind(prime, debt, profitability) ~ format, data = AVC02)

We can check the residual correlation matrix to see if there was a strong dependence between our measurements. The benefit of MANOVA is to be able to leverage this correlation, if any.

Code

cor(resid(model))

prime debt profitability

prime 1.00 -0.40 -0.54

debt -0.40 1.00 0.65

profitability -0.54 0.65 1.00

We can look at the global mean for each variable and the estimated mean differences for all groups, including the reference which is omitted. It’s easy to see that the mean differences sum to zero.

Code

dummy.coef(model)

Full coefficients are

(Intercept): prime 1.280511

debt 2.881521

profitability 2.597695

format: integrated note stand-alone note

prime -0.099261229 -0.013844563

debt 0.068479117 -0.059298660

profitability 0.127304965 0.002304965

(Intercept):

format: modified auditor report

0.113105792

-0.009180457

-0.129609929

Multivariate analysis of variance

Next, we compute the multivariate analysis of variance table and the follow-up with the univariate functions. By default, we can add a multiplicity correction for the tests, using Holm-Bonferonni with option 'holm'. For the MANOVA test, there are multiple statistics to pick from, including Pillai, Wilks, Hotelling-Lawley and Roy. The default is Pillai, which is more robust to departures from the model hypothesis, but Wilks is also popular choice among practitioners.

Code

car::Manova(model, test ="Pillai")

Type II MANOVA Tests: Pillai test statistic

Df test stat approx F num Df den Df Pr(>F)

format 2 0.02581 0.55782 6 256 0.7637

Effect sizes

We can compute effect sizes overall for the MANOVA statistic using the correspondance with the \(F\) distribution, and also the individual effect size variable per variable. Here, the values returned are partial \(\widehat{\eta}^2\) measures.

Code

effectsize::eta_squared(car::Manova(model))

# Effect Size for ANOVA (Type II)

Parameter | Eta2 (partial) | 95% CI

-----------------------------------------

format | 0.01 | [0.00, 1.00]

- One-sided CIs: upper bound fixed at [1.00].

Code

# Since it's a one-way between-subject MANOVA, no partial measureeffectsize::eta_squared(model, partial =FALSE)

Warning: Argument `effectsize_type` is deprecated. Use `es_type` instead.

# Effect Size for ANOVA (Type I)

Response | Parameter | Eta2 | 95% CI

---------------------------------------------------

prime | format | 0.01 | [0.00, 1.00]

debt | format | 2.23e-03 | [0.00, 1.00]

profitability | format | 0.02 | [0.00, 1.00]

Post-hoc analyses

We can continue with descriptive discriminant analysis for the post-hoc comparisons. To fit the model using the lda function from the MASS package, we swap the role of the experimental factor and responses in the formula. The output shows the weights for the linear combinations.

Code

MASS::lda(format ~ prime + debt + profitability,data = AVC02)

Call:

lda(format ~ prime + debt + profitability, data = AVC02)

Prior probabilities of groups:

integrated note stand-alone note modified auditor report

0.3030303 0.3409091 0.3560606

Group means:

prime debt profitability

integrated note 1.181250 2.950000 2.725000

stand-alone note 1.266667 2.822222 2.600000

modified auditor report 1.393617 2.872340 2.468085

Coefficients of linear discriminants:

LD1 LD2

prime 0.5171202 0.16521149

debt 0.6529450 0.97286350

profitability -1.2016530 -0.04412713

Proportion of trace:

LD1 LD2

0.9257 0.0743

Interpretation of these is beyond the scope of the course, but you can find information about linear discriminant analysis in good textbooks (e.g., Chapter 12 of Mardia et al., 2024).

Model assumptions

The next step before writing about any of our conclusions is to check the model assumptions. As before, we could check for each variable in turn whether the variance are the same in each group. Here, we rather check equality of covariance matrix. The test has typically limited power, but unfortunately is very sensitive to departure from the multivariate normality assumption, so sometimes rejection are false positive.

Here, there is a smallish \(p\)-value, so weak evidence against equality of covariance matrices. The data were generated from normal distribution, but the small \(p\)-value is an artifact of the rounding of the Likert scale.

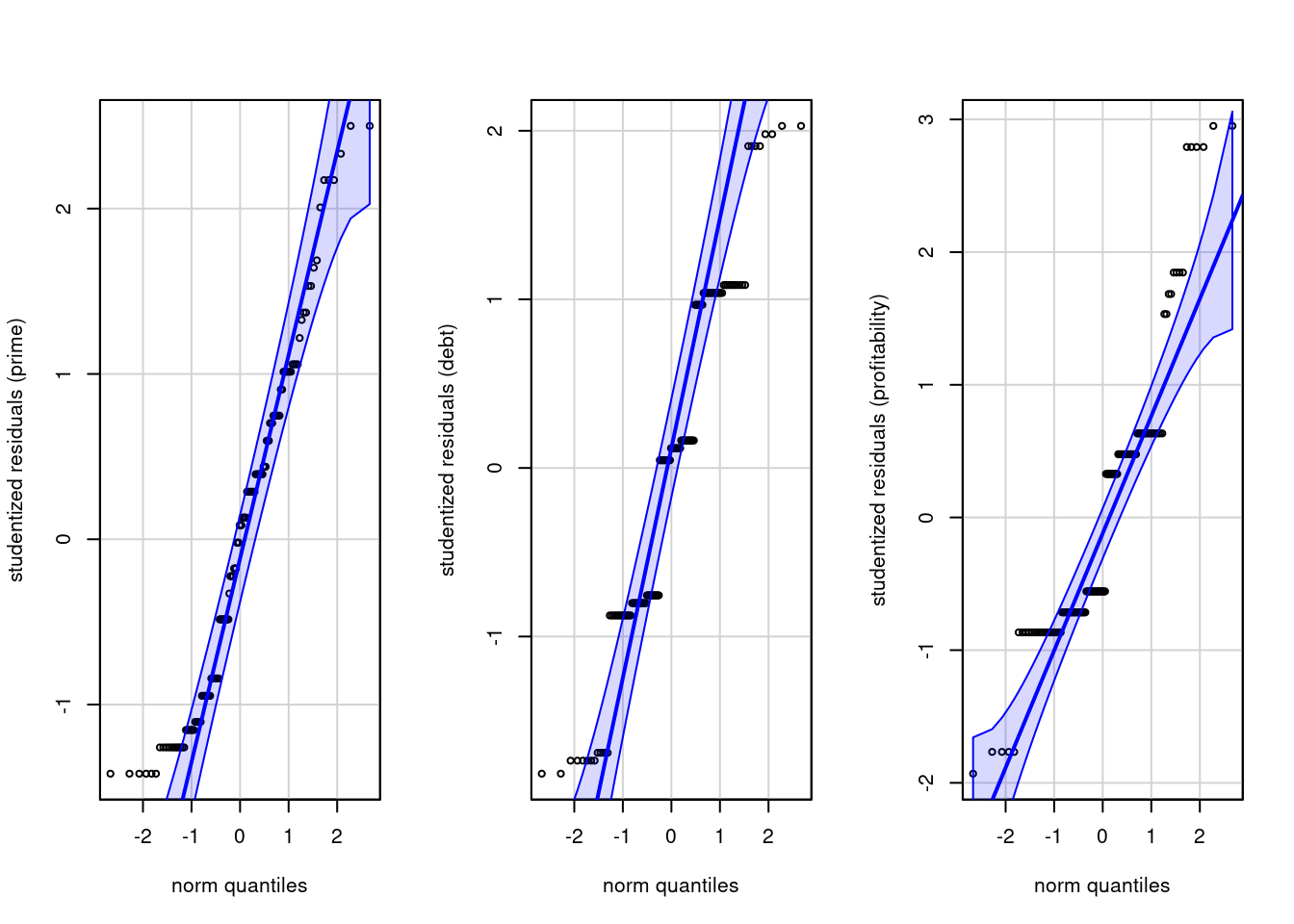

We can test the normality assumption using univariate quantile-quantile plots or tests of normality, including Shapiro-Wilks.

Code

par(mfrow =c(1,3)) # one row, 3 columns for plot layoutcar::qqPlot(rstudent(model)[,1], id =FALSE, # don't flag outliersylab ="studentized residuals (prime)")car::qqPlot(rstudent(model)[,2], id =FALSE, ylab ="studentized residuals (debt)")car::qqPlot(rstudent(model)[,3], id =FALSE, ylab ="studentized residuals (profitability)")

We see severe rounding impacts for debt and profitability. There is little to be done about this, but the sample size are large enough that this shouldn’t be too much a concern.

We can also test the multivariate normality assumption. The latter supposes that observations in each group have the same mean. To get this, we detrend using multivariate linear model by subtracting the mean of each group. Thus, our input is the matrix of residuals, which must be transposed for the function to work.

Code

mvnormtest::mshapiro.test(U =t(resid(model)))

Shapiro-Wilk normality test

data: Z

W = 0.96982, p-value = 0.004899

There is (unsurprisingly) strong evidence against multivariate normality, but it matters less due to sample size. This is a consequence of the discrete univariate measurements, which explain rejection of the null (for data to be multivariate normal, each of the response must be univariate normal and the dependence structure must also match.

Since assumptions are doubtful, we recommend using Pilai’s trace as test statistic for the MANOVA.

References

Anandarajan, A., Viger, C., & Curatola, A. P. (2002). An experimental investigation of alternative going-concern reporting formats: A Canadian experience. Canadian Accounting Perspectives, 1(2), 141–162. https://doi.org/10.1506/5947-NQTC-C3Y5-H46N

Mardia, K. V., Kent, J. T., & Taylor, C. C. (2024). Multivariate analysis (Wiley, Ed.; 2nd ed.).

Source Code

---title: "Multivariate analysis of variance"type: docseditor_options: chunk_output_type: console---The data presented in this example vignette is inspired by a study from @Anandarajan:2002, who looked at the impact of communication means through different disclosure format on the perceived risk of organization on the brink of bankruptcy in accountancy. There is a single between-subject factor for the disclore format, and three measures of the performance, ratings for the interest rate premium assessed, for the ability to service debt and that to improve profitability.## Data We first load the data from the package and inspect the content.```{r}data(AVC02, package ="hecedsm")str(AVC02)xtabs(~ format, data = AVC02)```The data are unbalanced by condition. In general, we need them to be roughly balanced to maximize power. The `manova` function will not be usable unless data are balanced, and we need to enforce sum-to-zero constraints to get sensible outputs. After this is done, we can fit the multivariate linear model with `lm` by binding columns on the left of the `~` sign to gather the response vectors.```{r}options(contrasts =c("contr.sum", "contr.poly"))model <-lm(cbind(prime, debt, profitability) ~ format, data = AVC02)```We can check the residual correlation matrix to see if there was a strong dependence between our measurements. The benefit of MANOVA is to be able to leverage this correlation, if any.```{r}#| eval: false#| echo: truecor(resid(model))``````{r}#| eval: true#| echo: falseround(cor(resid(model)), 2)```We can look at the global mean for each variable and the estimated mean differences for all groups, including the reference which is omitted. It's easy to see that the mean differences sum to zero.```{r}dummy.coef(model)```## Multivariate analysis of varianceNext, we compute the multivariate analysis of variance table and the follow-up with the univariate functions. By default, we can add a multiplicity correction for the tests, using Holm-Bonferonni with option `'holm'`. For the MANOVA test, there are multiple statistics to pick from, including `Pillai`, `Wilks`, `Hotelling-Lawley` and `Roy`. The default is `Pillai`, which is more robust to departures from the model hypothesis, but `Wilks` is also popular choice among practitioners.```{r}car::Manova(model, test ="Pillai")```## Effect sizesWe can compute effect sizes overall for the MANOVA statistic using the correspondance with the $F$ distribution, and also the individual effect size variable per variable. Here, the values returned are partial $\widehat{\eta}^2$ measures.```{r}effectsize::eta_squared(car::Manova(model))# Since it's a one-way between-subject MANOVA, no partial measureeffectsize::eta_squared(model, partial =FALSE)```## Post-hoc analysesWe can continue with descriptive discriminant analysis for the post-hoc comparisons. To fit the model using the `lda` function from the `MASS` package, we swap the role of the experimental factor and responses in the formula. The output shows the weights for the linear combinations.```{r}MASS::lda(format ~ prime + debt + profitability,data = AVC02)```Interpretation of these is beyond the scope of the course, but you can find information about linear discriminant analysis in good textbooks [e.g., Chapter 12 of @Mardia.Kent.Taylor:2024].## Model assumptionsThe next step before writing about any of our conclusions is to check the model assumptions. As before, we could check for each variable in turn whether the variance are the same in each group. Here, we rather check equality of covariance matrix. The test has typically limited power, but unfortunately is very sensitive to departure from the multivariate normality assumption, so sometimes rejection are false positive.```{r}with(AVC02,biotools::boxM(cbind(prime, debt, profitability),grouping = format))```Here, there is a smallish $p$-value, so weak evidence against equality of covariance matrices. The data were generated from normal distribution, but the small $p$-value is an artifact of the rounding of the Likert scale. We can test the normality assumption using univariate quantile-quantile plots or tests of normality, including Shapiro-Wilks.```{r}par(mfrow =c(1,3)) # one row, 3 columns for plot layoutcar::qqPlot(rstudent(model)[,1], id =FALSE, # don't flag outliersylab ="studentized residuals (prime)")car::qqPlot(rstudent(model)[,2], id =FALSE, ylab ="studentized residuals (debt)")car::qqPlot(rstudent(model)[,3], id =FALSE, ylab ="studentized residuals (profitability)")```We see severe rounding impacts for debt and profitability. There is little to be done about this, but the sample size are large enough that this shouldn't be too much a concern.We can also test the multivariate normality assumption. The latter supposes that observations in each group have the same mean. To get this, we detrend using multivariate linear model by subtracting the mean of each group. Thus, our input is the matrix of residuals, which must be transposed for the function to work.```{r}mvnormtest::mshapiro.test(U =t(resid(model)))```There is (unsurprisingly) strong evidence against multivariate normality, but it matters less due to sample size. This is a consequence of the discrete univariate measurements, which explain rejection of the null (for data to be multivariate normal, each of the response must be univariate normal and the dependence structure must also match.Since assumptions are doubtful, we recommend using Pilai's trace as test statistic for the MANOVA.